Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. Our research is independent and unbiased.

Editorial Note: This article was researched with AI assistance and reviewed by licensed veterinary and insurance professionals before publication.

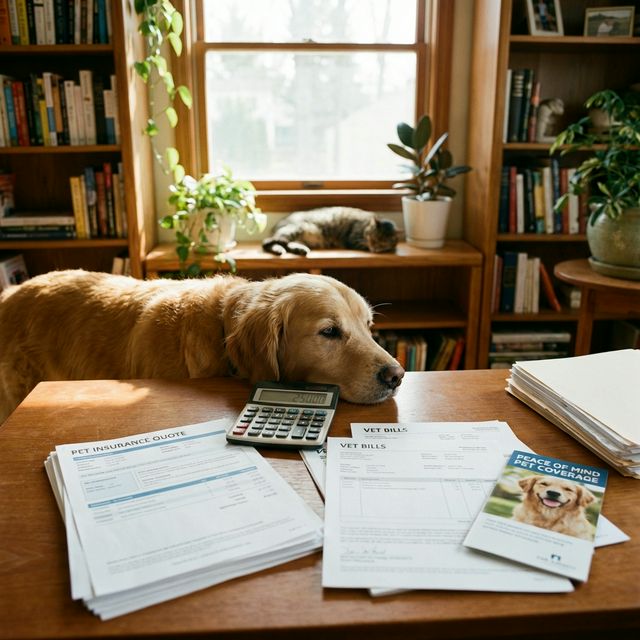

How Much Does Dog Insurance Actually Cost in 2026?

As an ER vet tech of 15 years, I break down the real costs of dog insurance in 2026—and show you how to protect your pup without going broke.

Pet Insurance Guide Research Team

Independent Analysts

In my 15 years working triage at a 24/7 animal ER, the worst part of my job isn’t the blood, the ruptured anal glands, or the 3 AM shifts. It’s handing an owner an estimate for a life-saving surgery, watching their face fall, and hearing them say, “We can’t afford that.”

We call it economic euthanasia, and it shatters my heart every single time.

You’re here wondering what dog insurance actually costs in 2026, and if it’s worth it. Let me give you the blunt, honest truth from the other side of the exam table.

The Real Talk on Monthly Costs

Most owners I talk to are paying between $30 and $80 a month for a solid accident and illness policy. If you just want coverage for the dumb things dogs do—like swallowing a squeaker toy whole—an accident-only plan is about $10 to $25 a month.

But why does your quote look different? It comes down to three things.

Factor 1: Breed (The Genetic Lottery)

I love Frenchies, but structurally, they are a medical disaster. If you own a French Bulldog, an English Bulldog, or a giant breed like a Great Dane or Bernese Mountain Dog, you are going to pay top dollar (often well over $100/mo). Insurers know these dogs are highly likely to need spinal surgeries, hip replacements, or airway surgeries just so they can take a full breath of air without suffocating.

If you have a scruffy mixed breed, a Jack Russell, or a Shih Tzu, congratulations—your mutt’s sturdy genetics mean you’ll probably pay around $35 a month.

Factor 2: Age (Don’t Wait Until They’re Gray)

Insure your puppy the second you bring them home. At 8 weeks old, they are a blank slate and rates are dirt cheap. By the time they hit 3 to 6 years old, rates creep up. If you try to insure an 8-year-old senior dog who already has a limp and a cloudy eye, expect your premium to double or triple. Plus, anything they’ve already been seen for won’t be covered anyway.

Factor 3: Zip Code Matters

It costs a lot more to run a clinic in San Francisco or Manhattan than it does in rural Ohio. Our rent, our diagnostic equipment, and our staff salaries are higher in cities, which means our vet bills are higher. Your insurance premium is directly tied to the cost of vet care in your zip code.

The Medical Reality: Is It Worth It?

Let’s look at the math. If you pay $50 a month for 5 years, you’ve spent $3,000.

Now, let’s look at a Tuesday night in my ER:

- TPLO (ACL) Surgery: Your dog blows out their knee chasing a squirrel. We have to cut the tibia bone, rotate it, and screw a metal plate into it so they can walk again. That’s $3,000 to $6,000.

- Cancer Treatment: Chemotherapy and radiation to give you a few more good, pain-free years with your best friend. That’s easily $5,000 to $10,000.

- Foreign Body Surgery: Your Golden Retriever ate a corn cob. It’s rotting in their intestines, causing a deadly blockage. We have to slice their belly open, cut into the bowel, pull out the blockage, and flush the abdomen to prevent sepsis. That’s $2,000 to $5,000.

One single bad day pays for five years of premiums. It turns a tragic “I have to put him down” conversation into “Do whatever it takes to fix him.”

Insider Tips to Lower Your Bill

If money is tight, don’t skip insurance entirely—tweak your policy:

- Raise the deductible: If you have a decent savings account, bump your deductible from $250 to $500. This can drop your monthly premium by 20%.

- Drop the reimbursement rate: Covering 80% of a massive bill instead of 90% is still a lifesaver, and it lowers your monthly cost.

- Pay upfront: A lot of companies give a discount if you pay the annual premium all at once.

- Stack the discounts: Always ask if they have multi-pet, military, or employer discounts.

The Honest Truth

At the end of the day, pet insurance isn’t an investment you hope to make money on. It’s a shield. If a sudden $5,000 vet bill would force you into a devastating choice, pay the $40 or $50 a month. Do it for your own peace of mind, and do it so you never have to sit in a clinic room with someone like me, crying over a bill.

Related Articles

- Best Pet Insurance for French Bulldogs

- Pet Insurance Deductibles Explained

- Emergency Vet Costs 2026

- Embrace Pet Insurance Review

- Pre-Existing Conditions Guide

Related Guides

- Is Pet Insurance Worth It?

- Pet Insurance Cost Guide

- Insurance vs. Savings

- Best Pet Insurance for Dogs

- Best for Puppies

- Best Pet Insurance for Cats

Frequently Asked Questions

What is the average cost of dog insurance?

Honestly, you're looking at $30 to $80 a month for solid illness and accident coverage. If you just want a safety net for when they inevitably eat a sock, accident-only plans run $10 to $25.

Why is my dog's insurance so expensive?

Some breeds are walking vet bills. Frenchies and Great Danes are prone to massive genetic disasters, so insurers charge more. Add your dog's age and your local city's cost of living, and your premium reflects that reality.

How can I lower my pet insurance premium?

Bump your deductible up to $500 if you can handle the out-of-pocket hit, drop your reimbursement down to 80%, and pay the whole year upfront if they offer a discount.