Disclosure: This post contains affiliate links. We may earn a commission at no extra cost to you. Our research is independent and unbiased.

Editorial Note: This article was researched with AI assistance and reviewed by licensed veterinary and insurance professionals before publication.

Demystifying Your Payout: Using a Pet Insurance Reimbursement Calculator for Your Actual Vet Bill

As a vet tech of 15 years, I see owners panic over bills every day. Here is the blunt truth on how to calculate your pet insurance payout so you aren't surpr...

Pet Insurance Guide Research Team

Independent Analysts

2026 Market Update: This article has been reviewed to reflect the latest veterinary costs and insurance market conditions for 2026.

You’ve just left our clinic. Your dog is finally stable, the IV catheter is out, and they’re resting in the back. But now you’re standing at the front desk looking at a massive emergency bill, and your heart is sinking.

I’ve been a vet tech for 15 years, and I see this panic every single shift. You have pet insurance, which is a relief, but in that moment of exhaustion, the last thing you want to do is guess how much of a $2,000 bill you’re actually getting back. The gap between the total we ring up and the final check you receive in the mail can be confusing.

Let’s cut through the insurance jargon. You don’t need a fancy “pet insurance reimbursement calculator” app. You just need to know the basic math of your policy so you aren’t left high and dry.

The Three Pillars of Your Payout

Before we can calculate anything, you need to understand the three basic terms that define your policy. These numbers determine your monthly premium and exactly how much you get back when disaster strikes.

1. Your Annual Deductible

This is your share of the pain before the insurance steps in. If you chose a $250 deductible, you are on the hook for the first $250 of covered care each year. Once you hit that number, the insurance company starts doing its job.

- How it works: Most plans use an annual deductible. If you drop $250 on a January visit, your deductible is met for the rest of the year.

- The Trade-off: Lower deductibles mean a higher monthly bill. Higher deductibles lower your monthly premium.

- The Exception: Some companies, like Trupanion, use a per-condition deductible. You pay a deductible once for a specific illness (like diabetes) for the lifetime of the pet. It’s great for chronic issues, but it can get expensive if your pet is prone to lots of unrelated random injuries.

2. Your Reimbursement Percentage

This is the cut the insurance company takes on after your deductible is met. The rest is your co-pay.

- How it works: If you have a 90% plan, they pay 90% of the remaining bill, and you eat the other 10%.

- Common Options: You’ll usually see 70%, 80%, or 90%.

- My Advice: Higher percentages mean a bigger safety net. When I see an owner facing a $6,000 bill for an emergency bloat surgery, that 90% reimbursement is what keeps them from considering economic euthanasia. It’s usually worth the extra monthly cost.

3. Your Annual Limit (Maximum Payout)

This is the absolute ceiling on what your insurance will pay out in a single year.

- How it works: Once your reimbursements hit this cap, you are paying 100% of any other bills until your policy renews.

- Common Options: Limits range from $2,500 up to unlimited.

- Why I Hate Low Limits: A $5,000 limit sounds like a ton of money until your dog eats a sock and needs exploratory surgery to remove it before the intestines go necrotic. I’ve seen it a hundred times, and it easily blows past $5,000. If you can afford an unlimited plan, get it. It stops you from ever having to make a life-or-death choice based on an arbitrary benefit cap.

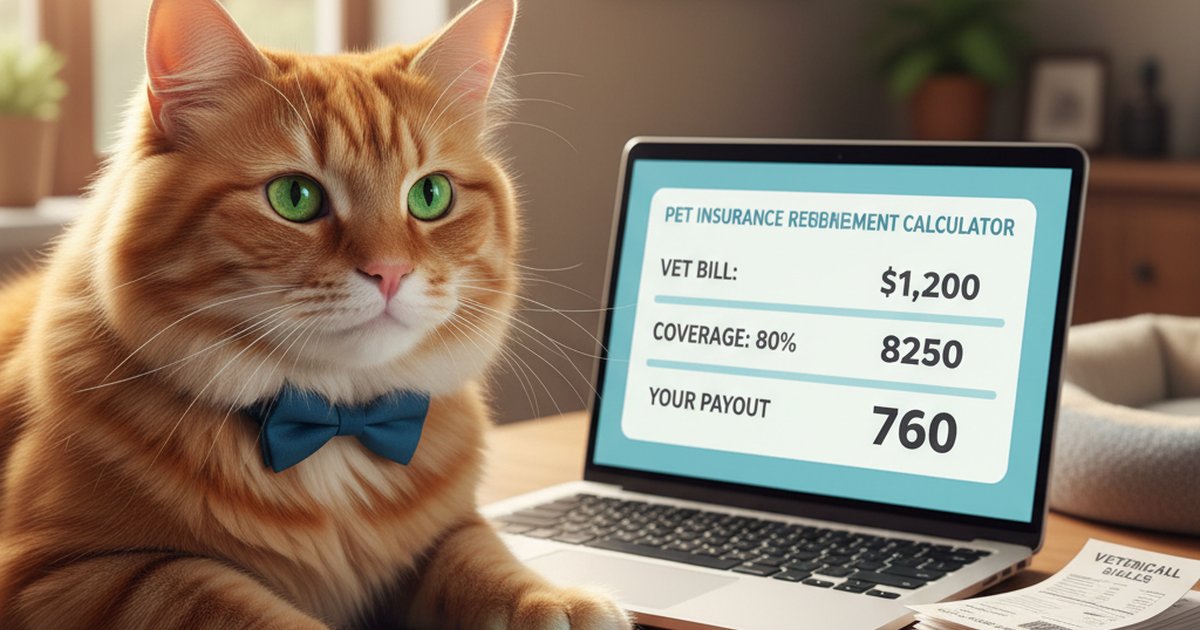

Let’s Calculate: A Real-World Emergency Bill

Let’s say your dog, Max, came into our ER. He’s been vomiting profusely and is completely lethargic. We had to do a full blood panel, x-rays to check for blockages, and get him on IV fluids to rehydrate him.

Your Policy:

- Annual Deductible: $250

- Reimbursement: 90%

- Annual Limit: $15,000

The Actual Vet Bill:

- Emergency Exam Fee: $150

- X-rays (3 views): $300

- Full Blood Panel: $200

- IV Catheter, Fluids & Hospitalization: $400

- Anti-nausea Medication (Cerenia): $75

-

- Total Vet Bill: $1,125

Here is the exact math to figure out your payout.

Step 1: Strip out what isn’t covered

Most basic policies refuse to cover the exam fee. So right off the bat, we subtract that $150.

- Total Bill: $1,125

- Subtract Non-Covered Exam Fee: -$150

- Total Covered Costs: $975

Step 2: Take out the deductible

Assuming this is Max’s first big issue this year, you owe your full $250 deductible.

- Total Covered Costs: $975

- Subtract Annual Deductible: -$250

- Amount Eligible for Reimbursement: $725

- (The good news? Your deductible is met for the rest of the year!)

Step 3: Apply the reimbursement rate

Now the insurance company kicks in their 90%.

- Amount Eligible for Reimbursement: $725

- Multiply by Reimbursement Percentage: x 90% (or 0.90)

- Your Final Reimbursement: $652.50

Step 4: Your Real Out-of-Pocket Cost

So, what is the actual hit to your bank account? It’s everything the insurance didn’t cover.

- Total Vet Bill: $1,125

- Subtract Your Reimbursement: -$652.50

- Your Final Out-of-Pocket Cost: $472.50

You are paying the $150 exam fee, the $250 deductible, and your 10% share ($72.50).

Different Companies, Different Math

The basic math above works for most companies, but a few have completely different setups that you need to be aware of.

- Trupanion: In our clinic, we love them because they have software that pays us directly at checkout. You just pay your portion and leave. It saves you from floating a massive charge on your credit card while you wait weeks for a check.

- Nationwide: They have some plans that work on a “benefit schedule.” This means they pay a flat, pre-determined rate for a specific diagnosis, no matter what we actually charge you. It can be incredibly frustrating for owners when an emergency treatment costs $1,500 but the schedule only allows for an $800 payout.

- Embrace: They offer a “Healthy Pet Deductible.” For every year you don’t file a claim, your deductible drops by $50. It’s a nice perk when you finally do need to use the insurance.

Final Advice: Plan for the Worst

I’ve held the paws of too many pets while their owners cried over finances in the lobby. Please, don’t just pick the cheapest monthly premium. Do the math. Figure out what happens if your dog tears an ACL or needs cancer treatment. Pick a policy that gives you the peace of mind to look at us and say, “Do whatever it takes,” without panicking about the cost.

Related Guides

- Is Pet Insurance Worth It?

- Pet Insurance Cost Guide

- Insurance vs. Savings

- Best Pet Insurance for Dogs

- Best for Puppies

- Best Pet Insurance for Cats

Frequently Asked Questions

What is a pet insurance deductible?

It’s the chunk of change you have to pay out of your own pocket before the insurance company even looks at your claim. Most plans have an annual deductible, meaning you only have to hit that number once a year. After that, they start sharing the load.

Does the reimbursement rate apply before or after the deductible?

Always after. First, we take your total covered bill and subtract your deductible. Whatever is left over is what your reimbursement percentage applies to. That’s the amount you actually get a check for.

Are exam fees covered by pet insurance?

Honestly, most basic accident and illness plans don't cover the exam fee—which can be anywhere from $50 to $200 just to walk in the ER door. Providers like Lemonade or Embrace have add-ons that might cover it, but check your fine print. I always tell owners to expect to pay the exam fee out of pocket.